Written by Arundhati Sampath

If you are planning a startup journey or already in the middle of one it’s really important to take a step back and think through your personal finances. Startup life can be unpredictable, and not having your finances in order can add a lot of unnecessary stress and affect not just your personal life but also to how you run your company. Having a solid financial plan gives you the peace of mind to focus on building and growing your startup. This is the reason I built Planwell, to help people plan their finances for major life decisions.

Here is the definitive guide for the major financial decisions every founder should think about before and during the early startup phase.

Decide how long you will commit to your startup

It is wise to give yourself a certain period of time to work on your startup and evaluate whether it will work out. Set clear milestones that you need to achieve within a certain period of time.

These milestones could include things like:

- hitting a certain number of paying customers

- achieving product-market fit

- raising a funding round

This time-bound approach creates focus and prevents the startup from becoming a never-ending project. It also helps you plan your finances better.

How does your stage of life affect this decision?

Your financial strategy will almost certainly differ depending on where you are in life. Early career founders often have lower fixed costs and may still be on a parent’s health insurance plan, which makes a shorter runway more manageable. Founders with families face higher fixed costs such as childcare, schooling and family health insurance. However, they may also have a higher level of savings accumulated and potentially a partner whose income or insurance provides a buffer. Take stock of your full picture and try to maintain a higher personal reserve before committing fully.

Analyze your cash flow and budget requirements

Before leaving your salaried job, analyze your personal cash flow and understand how much you spend every month. In particular, try to figure out the discretionary expenses that you could cut while you are working on the startup.

What can you do to prepare financially while still in a W2 role?

If you have the leeway, try to keep your fixed costs low. If you have the dream of doing a startup down the line, do not buy the most expensive home and do not max out your lifestyle, even if you can afford it. The flexibility you preserve now becomes the runway you have later.

What are your health insurance options as a founder?

Unless you have a spouse or parent whose health insurance you can rely on, you need to figure out health insurance options and budget for them before you make the leap. You can purchase coverage through the Individual Marketplace via the Affordable Care Act (ACA). Typical monthly premiums vary by age and state:

- Bronze plans: ~$380 to $785

- Silver plans: ~$403 to $1,036

- Gold plans: ~$478 to $1,135

Early-stage teams sometimes use services like Take Command Health to navigate options.

Hat tip: Try to be conservative with expenses and just spend what is needed rather than maintaining a full salaried budget.

Estimate whether you have funds to cover your budget

How many months or years of runway do you have to cover your budget? Does this match the period of time you gave yourself to work on your startup and take it to the next level?

Number of months of runway = Funds available / monthly budget.

This calculation determines whether you can bootstrap or whether you need other income sources.

How can you model your personal financial runway before quitting your job?

Start with the calculation above, but keep in mind that most founders underestimate costs like healthcare, quarterly taxes and irregular expenses.

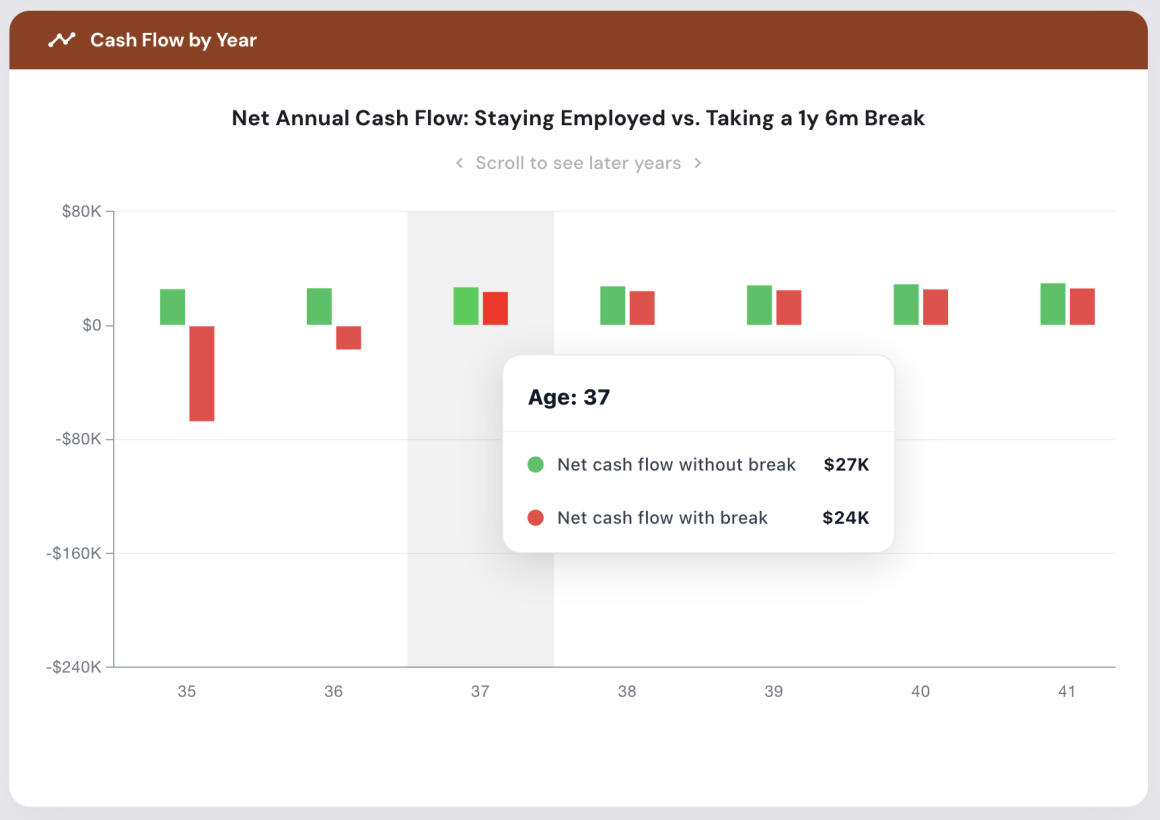

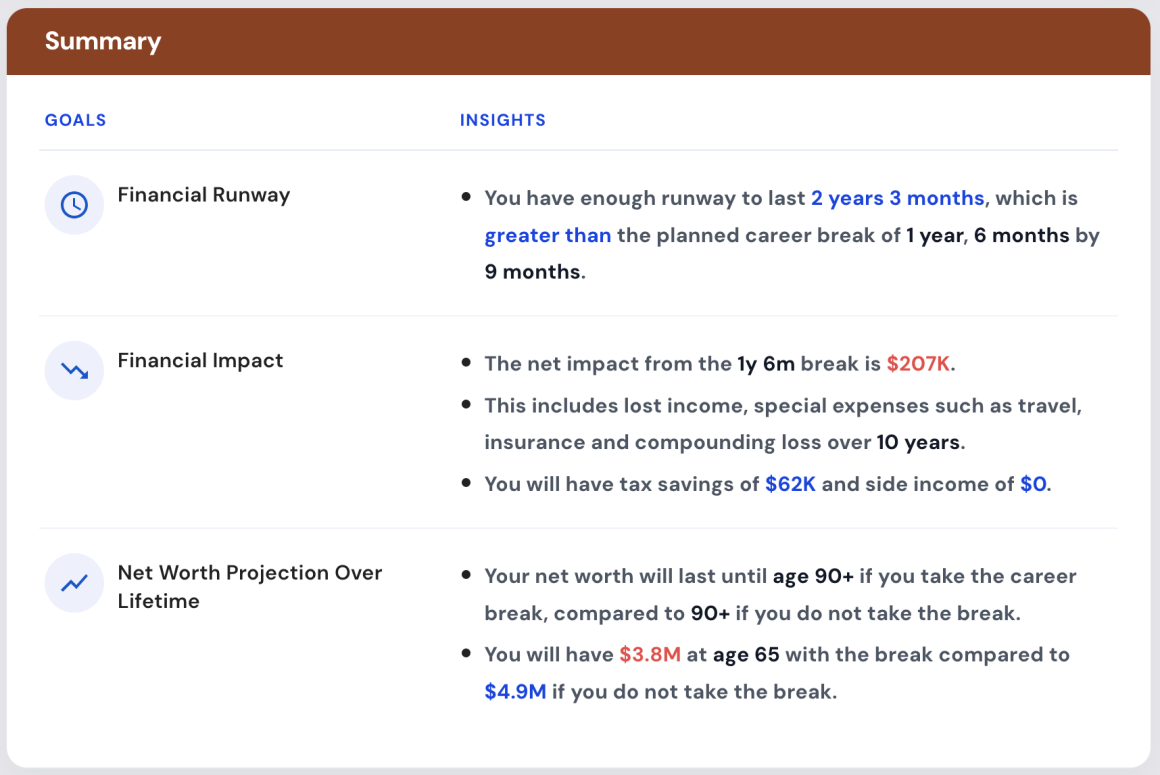

A tool like Planwell’s Career Break Planner lets you input your exact income, expenses, assets and goals and stress-test your runway under different spending scenarios. You can also model how a major decision like buying a home changes how long your savings will last. Unlike a generic AI tool like ChatGPT, Planwell uses its own financial models and runs your exact numbers, so the output is specific to your situation rather than a general answer that could apply to anyone.

Build a founder-sized emergency fund

The standard advice, three to six months of expenses in reserve, was written for people with stable salaries. As a founder, aim for at least twelve months of personal expenses in liquid savings. Keep this separate from whatever you have allocated to the business. This will help ensure that an unexpected expense or a delayed funding round does not force a bad business decision.

If You Don’t Have Enough Savings, Consider Your Options

- Raise funding: Raise a pre-seed or seed round so you can pay yourself a modest founder salary.

- Work on the startup part-time: Keep your full-time job and build the startup until you reach early traction.

- Take contract or part-time work: Many founders do consulting or freelance work to support themselves while building.

- Reduce expenses: Cut costs and build additional savings before going full-time.

Review legal and tax obligations

When you set up your startup in the US, you have to make sure to file Form 83(b) which lets you pay taxes upfront on the restricted stocks at the value at grant rather than when the stock vests. This is because stocks appreciate upon vesting and you will have to pay ordinary income tax upon vesting. The form 83(b) has to be filed within 30 days of the grant and this is absolute. Missing filing the 83(b) within this 30-day period is usually irreversible and can lead to massive unexpected tax bills. Set a calendar reminder the day you sign your founding documents.

What are your retirement savings options as a self-employed founder?

As much as possible, do not deplete your retirement funds while building your startup. As a self-employed founder you have access to several tax-advantaged vehicles:

- Solo 401K: For self-employed individuals or owner-only businesses. You can contribute $24,500 in 2026 with a catch-up opportunity from age 50.

- SEP IRA: A tax-deferred contribution plan for self-employed individuals and small business owners. You can contribute up to 25% of your compensation,up to a maximum of $72,000 in 2026.

- Simple IRA: For small businesses with fewer than 100 employees. Requires an employer match of 3%. Contribution limits in 2026 are $18,000.

Understand your tax position as a self-employed founder

Your tax obligations depend on how your business is structured and how you pay yourself. If you’re operating as a sole proprietor, LLC, or partnership, taxes typically aren’t withheld automatically, and you may need to make quarterly estimated tax payments. Depending on your structure, you may also owe self-employment tax. By contrast, founders of C-Corporations who pay themselves a salary generally receive a W-2, with payroll taxes withheld just like any other employee. As a starting point, many founders set aside 25–35% of income for taxes, although the right amount depends on your income level and state of residence. Before choosing an entity structure, speak with a CPA who works with startups. The decision can have long-term implications for taxes, fundraising, and equity compensation.

Separate personal and company finances

It is wise to get a separate bank account for the business and not mix your personal and professional accounts. Even if you are the one funding the business, having a separate account helps you track how much you are actually spending on the business.

Think Carefully About Bootstrapping

Bootstrapping can be a great way to maintain ownership, but it also concentrates risk. Avoid putting all your personal assets into the company. Instead, allocate a specific budget for bootstrapping.

Tie that budget to milestones, such as:

- Building the first MVP

- Testing 5 different product ideas

- Finding product-market fit

- Raising an angel round

Consider part-time or side gig income

Even if you go full-time, you may want to consider part time or contract work on the side if finances are a crunch. You can consider consulting, contract work or freelance projects. This income can extend your personal runway while you are working on your startup.

Plan your founder salary if you have raised funding

Once you have raised funding, the question of how to pay yourself becomes more structured. Here is what founders typically do.

When should you start paying yourself?

Most founders begin paying themselves once the company raises funding or the business generates consistent revenue. The goal is not to match a big tech salary but to cover living expenses so you can focus fully on the company.

How much should you pay yourself?

Founder salaries typically depend on the funding stage and location. Many early-stage founders pay themselves enough to cover basic living expenses, often in the range of $70k to $120k in expensive cities, though this varies widely.

Investors generally expect founders to live comfortably but not extravagantly. Investors do not want you to be anxious and distracted due to money troubles, and encourage founders to take a decent salary that helps support their living expenses but otherwise want you to deploy all your resources into growing the business.

Think about equity as part of your personal finances

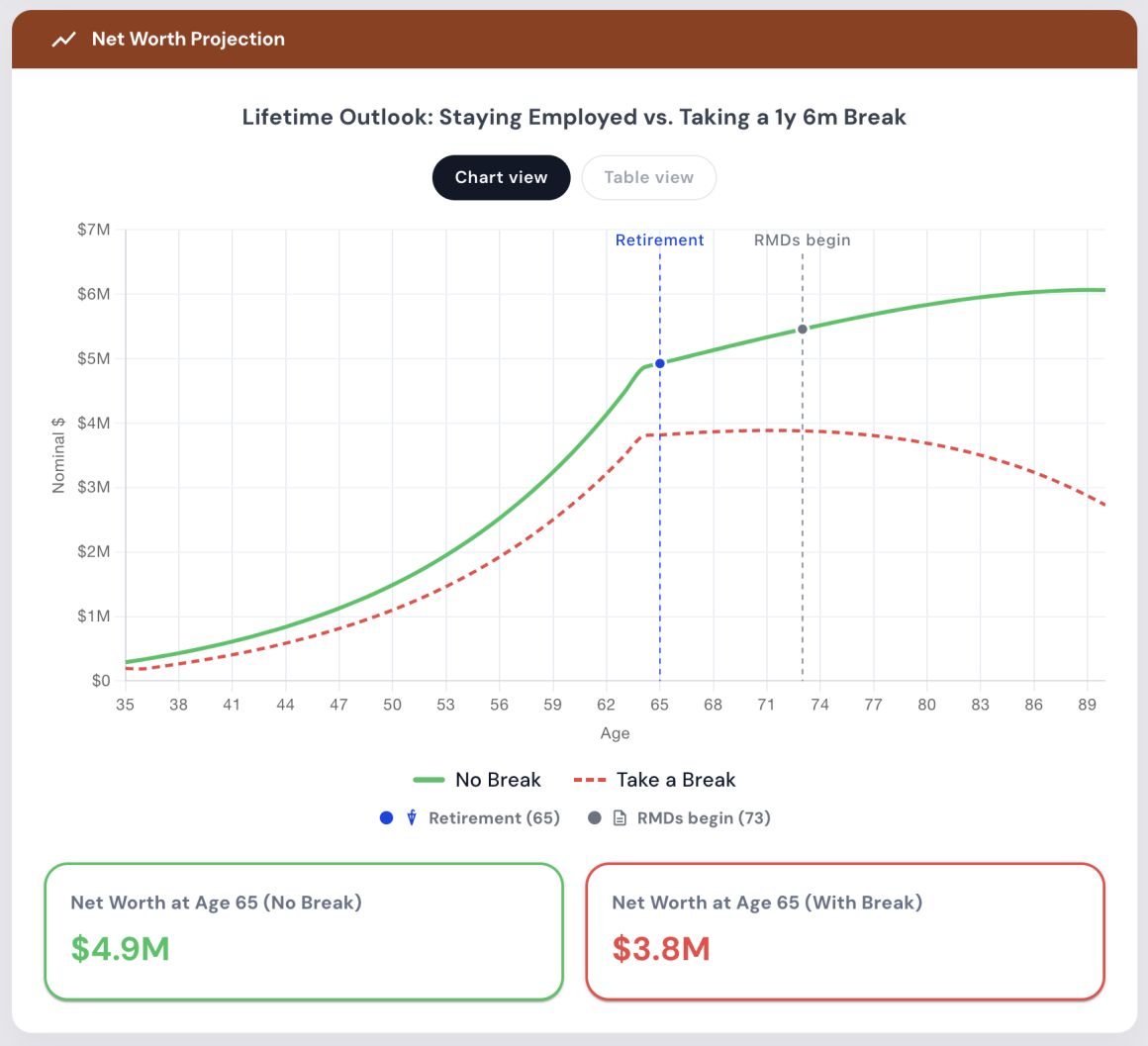

Your equity stake may represent the majority of your theoretical net worth on paper. It is also completely illiquid and might end up being worth nothing. Planwell’s lifetime financial projection shows your actual net worth at every stage of life, which is a useful reality check when equity makes your paper wealth look larger than your actual financial position. Plan your personal finances as if equity does not exist: maintain your savings, keep contributing to retirement, manage your fixed costs, and treat equity as optionality rather than income.

Protect your personal credit

Your credit score matters more as a founder than it ever did as an employee. Business credit lines and financing can touch it. Keep personal and business spending cleanly separated, pay personal obligations on time even when business finances are tight, and avoid personal guarantees until you fully understand what you are signing.

Plan around major life events

Buying a home, having a child, supporting an aging parent. These do not pause because you are building a company, and each one can materially change your personal runway overnight. Founders make the mistake of treating these as separate from their startup finances whereas they are deeply connected. Planwell is built for exactly this: you can run what-if scenarios to see how a single major decision like taking on a mortgage ripples through your cash flow, retirement timeline and other goals simultaneously, before you commit.

What to do if your startup fails financially

Startup failure is common and it is not something to be anxious about, but something to plan for financially. Often the startup experience can be a good value add to your resume and show that you have the drive and resourcefulness to handle high levels of ambiguity. So use your startup experiences and skills to obtain a leadership role at a company that values these skills.

In the process of building your startup, you may have done a lot of networking and met smart people. You can reach out to them and see if they can hire you or recommend you for a role. Many VC firms hire ex-founders and operators so do not forget to keep in touch with your VC friends.

The bottom line

Founders who navigate personal finances well tend to share one habit: they treat their own money with the same rigour they bring to their business. They know their runway, they separate their accounts, they plan for the costs that do not show up until they do.

The startup bet is already a bold one. The goal is to make sure your personal finances are stable enough that when hard decisions come, and they will, you are making them with a clear head. If you want to model your own situation, Planwell lets you input your exact income, expenses, assets and goals and get a personalized plan in minutes, without the generic advice that does not account for how founders actually live.

About the Author

Arundhati Sampath is the founder of Planwell, a financial planning tool designed to help people model life transitions such as startup journeys, career breaks, and early retirement.